Why early repayment of House Building Loan is bad for your financial health Part 2

- Tue Sep 21 18:30:00 UTC 2021

- In Personal Finance by Malhar Majumder

Key Takeaways:

- How much you actually pay after adjusting for inflation and tax

- The real rate of return for different loan tenures

- Taking the Decision making - "Pay or Stretch" house building loan

In Part 1 of the blog, we have created the grounds for making decision regarding early closure versus continuing a Home Loan. We calculated the actual quantum of money that we will have to pay to the Financial Institutions for different tenures of the loan. Then we introduced the key variables which was ignored in the earlier vanilla calculations. The dual impacts of Inflation and Tax Benefits. Now let's apply them to arrive at some numbers for our protagonist Mr Niraj.

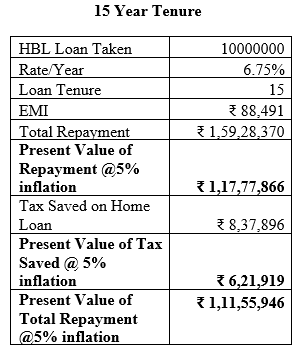

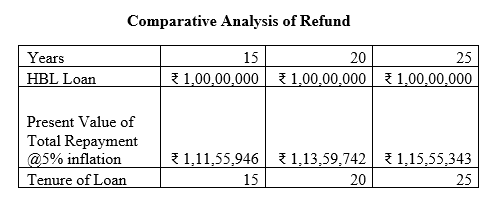

After taking inflation and income tax into consideration, the real rupee getting returned over 15 years is approximately Rs 1.12 crores only against a loan of 1.00 cores.

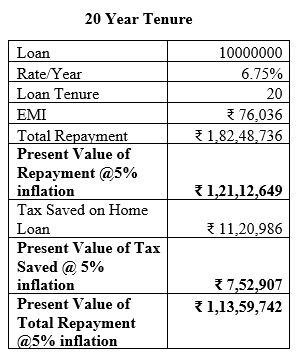

After taking inflation and income tax into consideration, the real rupee getting returned over 20 years is approximately Rs 1.14 crores only against a loan of 1.00 cores. An extra amount of 2 Lakh in 5 years.

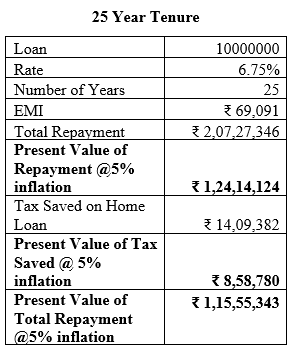

After taking inflation and income tax into consideration, the real rupee getting returned over 25 years is approximately Rs 1.16 crores only against a loan of 1.00 cores. An extra amount of 4 Lakh in 10 years if we compare with a 15 years tenure.

"A real interest rate is an interest rate that has been adjusted to remove the effects of inflation to reflect the real cost of funds to the borrower and the real yield to the lender or to an investor.

Real Interest Rate = Nominal Interest Rate - Inflation (Expected or Actual)"

Source – Investopedia.com (https://www.investopedia.com/terms/r/realinterestrate.asp)

"The beginning of wisdom is the definition of terms."

- Socrates

The 3rd and penultimate part of the fact-finding mission may create more interesting possibilities. Stay tuned for more fun.

Read the 3rd & Final part of the article

Disclaimer: The data and information has been sourced from various domains available to the public. We have taken utmost care to represent the same as factually as has been made available. Please do not make any decisions based on our blogpost. Kindly check the data & information independently. For further guidance on finance and investment please reach out to our experts at Investaffairs.

If you have any Personal Finance query, do write to us

Categories

Recent Posts